You found a neighborhood you love. Maybe you have been driving past a house on Maple Street for three months, slowing down every single time. But here is where most first-time buyers hit a wall: they fall in love with a home before they understand what it actually takes to get approved for a mortgage. Missed documents. Unexpected credit issues. Confusion about down payments. These are not rare problems; they happen every day, and they delay or derail purchases that should have gone smoothly.

This complete home loan checklist for first-time buyers walks you through exactly what lenders review, what documents you need to gather, and what financial steps you should take before you ever submit an application. If you are buying in Germantown, Dayton, Middletown, or anywhere in southwestern Ohio, this guide is built for you.

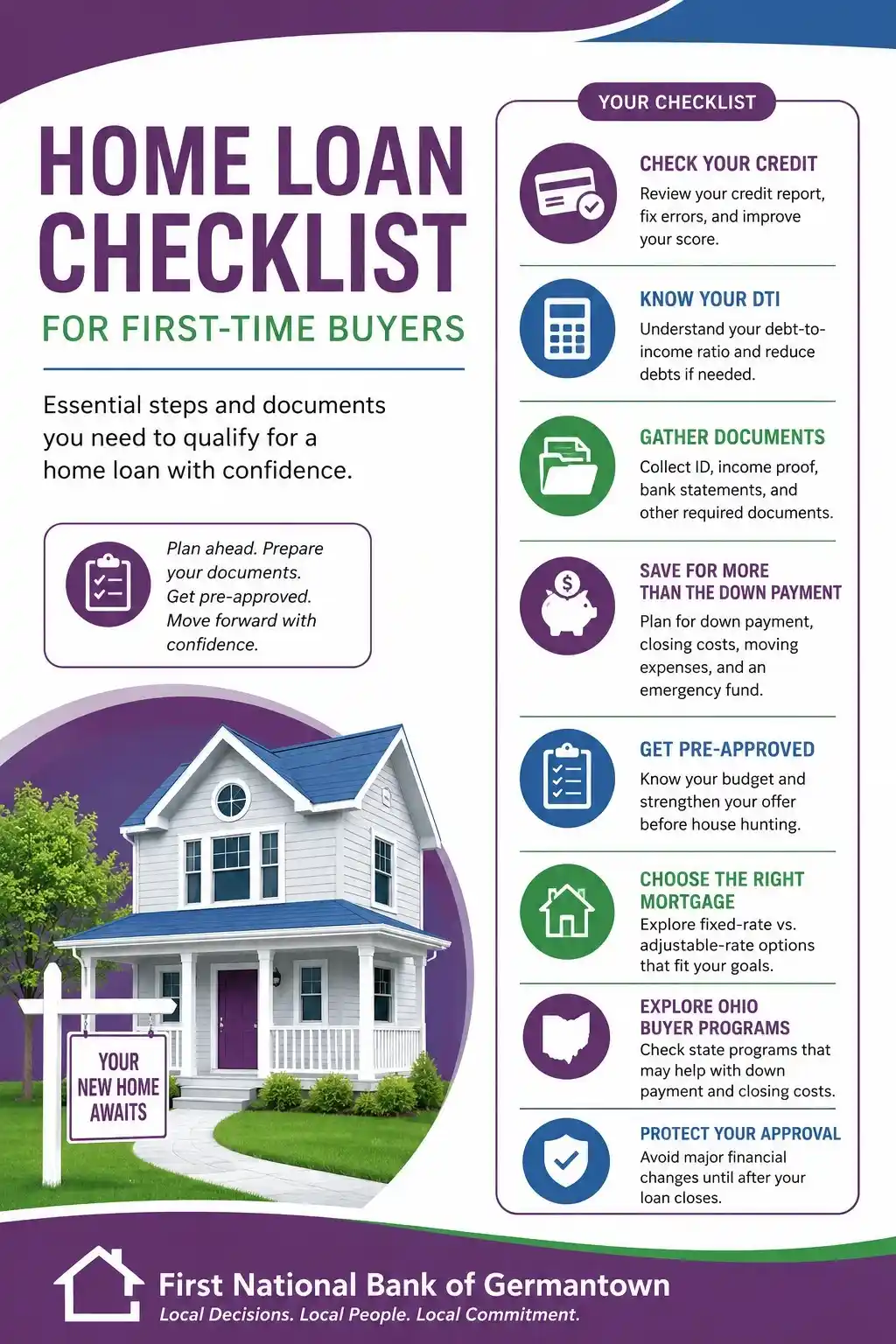

What Do You Need to Qualify for a Home Loan?

Most lenders will review your credit score, income, employment history, debt-to-income ratio, bank statements, down payment funds, and identification before approving a mortgage. Having these organized before you apply can speed up approval and reduce the chances of delays or denial.

Step 1: Pull Your Credit Report Before Anyone Else Does

Your credit score is one of the first things a lender will check. A stronger credit profile opens doors to better loan terms, while errors on your report, which are more common than most people expect, can create unnecessary obstacles.

Before you apply, do the following:

- Review your full credit report from all three bureaus (Equifax, Experian, TransUnion)

- Dispute any errors you find, even small ones

- Avoid opening new lines of credit in the months before applying

- Keep making on-time payments without exception

- Work on bringing down high credit card balances if your utilization is above 30%

Even a modest improvement in your score, made three to six months before applying, can meaningfully change what is available to you. This is one preparation step that is entirely within your control.

Step 2: Know Your Debt-to-Income Ratio

Your debt-to-income ratio, or DTI, compares what you owe each month to what you earn each month. Lenders use it to judge whether you can comfortably manage a mortgage payment on top of your existing obligations. Monthly debts that typically count in the calculation include auto loans, student loans, credit card minimum payments, personal loans, and any child support obligations.

If your DTI is higher than you would like, paying down specific debts before applying for revolving credit can improve your options. This is worth calculating on your own before a lender does it, so there are no surprises.

Step 3: Gather Every Document on This Mortgage Checklist

Incomplete paperwork is one of the most common reasons mortgage applications slow down or stall. Lenders are not trying to make the process difficult; they are required to verify specific information, and they cannot move forward without it.

Here is what most lenders will ask for:

Personal Identification

- Government-issued photo ID (driver’s license or state ID)

- Social Security number

Income Verification

- Two to three recent pay stubs

- W-2 forms from the past two years

- Federal tax returns from the past two years

- Documentation of any bonus, commission, or overtime income

Employment Information

- Employer name, address, and contact information

- Full employment history covering the past two years

- A letter of explanation if you changed jobs recently

Asset Documentation

- Checking and savings account statements (typically two to three months)

- Investment or brokerage account statements

- Retirement account balances

Additional Documents If They Apply to Your Situation

- Profit and loss statements or Schedule C forms if you are self-employed

- Rental income documentation

- A gift letter if any portion of your down payment is coming from a family member

- Divorce decree or separation agreement, if applicable

Gathering these items before you start the process removes one of the biggest friction points in getting approved.

Step 4: Understand What You Actually Need to Save

One of the most persistent myths in home buying is that you need a 20% down payment. While putting more down has advantages, many qualified buyers have options that require significantly less up front.

That said, your savings plan should account for more than just the down payment. A realistic first-time buyer savings target includes:

- Down payment varies by loan program and lender

- An earnest money deposit is typically required when you make an offer

- Closing costs generally range from 2% to 5% of the loan amount

- Moving expenses easy to forget, impossible to avoid

- Post-closing emergency fund, this one matters more than people expect

That last point deserves its own step.

Step 5: Build an Emergency Fund Before You Close

Homeownership comes with costs that renters rarely think about. The HVAC system does not care that you just closed on the house. A plumbing issue will not wait until you have had time to settle in. A well-prepared first-time buyer has at least two to three months of expenses in savings beyond the down payment and closing costs. This cushion is not just about peace of mind; it protects you from going into debt the moment something unexpected happens at home.

If your budget only stretches to the down payment right now, consider whether it makes sense to wait a few more months and build that reserve before buying.

Step 6: Get Pre-Approved Before You Fall in Love with a House

Mortgage pre-approval is a lender’s written estimate of how much you are likely to qualify to borrow, based on a preliminary review of your income, assets, and credit. It is not a guarantee, but it is the clearest signal you can give to sellers that you are a serious buyer.

Benefits of getting pre-approved early include:

- You know your actual budget before you start touring homes

- Your offer is more competitive in a market where sellers receive multiple bids

- You discover potential issues early, when there is still time to address them

- The full approval process moves faster because much of the work is already done

The documents you need for pre-approval largely overlap with the full mortgage application checklist above, so if you have already gathered those, you are most of the way there.

At First National Bank of Germantown, our lending team processes applications locally, meaning real people review your file and can answer your questions directly, not an automated system in another state.

Step 7: Understand Which Mortgage Type Fits Your Situation

Not every loan is designed for every buyer. Two of the most common options worth understanding are fixed-rate and adjustable-rate mortgages. Fixed-Rate Mortgage: The interest rate stays the same for the life of the loan. Monthly principal and interest payments are predictable from the first payment to the last. For buyers who plan to stay in a home long-term and want stable, budgetable payments, this is often the preferred choice.

Adjustable-Rate Mortgage (ARM) An ARM typically starts with a lower introductory rate that adjusts after a set period based on market conditions. This may appeal to buyers who plan to move or refinance within a few years, or who expect their income to grow before the rate adjusts. There is no universal right answer. The best option depends on your timeline, risk tolerance, and financial goals. This is exactly the kind of conversation worth having with a local lender who can walk through the numbers with you rather than offering a generic recommendation.

Step 8: Look Into Ohio First-Time Home Buyer Programs

Ohio offers programs through the Ohio Housing Finance Agency (OHFA) that may provide down payment assistance or favorable financing terms for eligible first-time buyers. Eligibility requirements vary based on income, purchase price, and the county where you are buying. Researching these programs early is worthwhile. If you qualify, assistance that reduces your upfront costs can make a meaningful difference in your overall financial picture after closing. A lender who works regularly with Ohio borrowers will know which programs are currently active and whether you are likely to qualify.

Step 9: Protect Your Approval. Do Not Make Major Financial Changes Before Closing

This is a step many buyers overlook after receiving pre-approval or even a conditional approval. Lenders often review your financial profile again before closing. A significant change between approval and closing can create serious complications.

Avoid the following until after your loan officially closes:

- Opening a new credit card or any other line of credit

- Financing furniture, appliances, or a vehicle

- Changing employers without speaking to your lender first

- Making large cash deposits that cannot be explained and documented

- Co-signing on someone else’s loan

These actions change the financial picture that your lender approved. Even if the changes seem minor, they can trigger additional reviews or, in some cases, put the loan at risk.

Common Mistakes That Delay First-Time Buyers

In our experience working with Ohio home buyers, most mortgage delays share a handful of root causes:

- Waiting too long to check credit, leaving no time to address issues

- Starting the home search before understanding the actual budget

- Underestimating closing costs and arriving at the finish line short on cash

- Skipping pre-approval and losing competitive offers as a result

- Taking on new debt during the process after pre-approval

- Focusing only on the monthly payment without accounting for taxes, insurance, and maintenance

Awareness of these patterns is half the battle. The other half is preparation, which is exactly what this checklist is designed to support.

Why First-Time Buyers in Ohio Choose a Local Lender

Large national lenders move a high volume of applications through automated systems. For straightforward transactions, that can work fine. But for first-time buyers, especially those with questions, unique income situations, or a desire to understand what they are signing, the experience often falls short.

Community banks work differently. At First National Bank of Germantown, we have been serving families and businesses in southwestern Ohio for over 150 years. Every mortgage decision is made locally by people you can actually speak with. We process applications here, close loans here, and service them here after closing.

That means if you have a question three months after you close, you are calling the same team that helped you get approved. You are not navigating an 800 number or waiting on a callback from a regional office. For families buying their first home in Germantown, Dayton, Middletown, Preble County, and the surrounding communities, that kind of continuity matters.

If you are ready to take the next step, our lending team is available to discuss your situation, walk through your mortgage options, and help you understand exactly where you stand. You can also connect with us directly. There is no pressure and no commitment required to have a conversation.

Frequently Asked Questions

Q.1 What documents are required for a mortgage application?

Most lenders require government-issued ID, recent pay stubs, W-2 forms, two years of tax returns, bank statements, and documentation of any other assets or income sources. If you are self-employed, additional documentation, such as profit and loss statements, will typically be required.

Q.2 What credit score do I need to qualify for a home loan?

Requirements vary by loan program and lender. In general, higher credit scores improve your options and the terms available to you. If your score is lower than you would like, spending a few months building it before applying is often worthwhile.

Q.3 How much money should I save before buying a home?

Plan for the down payment, closing costs (typically 2% to 5% of the loan amount), an earnest money deposit, moving expenses, and an emergency fund of at least two to three months of expenses. Buyers who only plan for the down payment often find themselves financially stretched after closing.

Q.4 What is the difference between mortgage pre-qualification and pre-approval?

Pre-qualification is an informal estimate based on information you provide verbally or online. Pre-approval involves a formal review of your documents and credit and carries significantly more weight with sellers. If you are serious about buying, pre-approval is the step that matters.

Q.5 Are there down payment assistance programs for Ohio first-time buyers?

Yes. The Ohio Housing Finance Agency offers programs that may reduce upfront costs for eligible buyers. Income limits, purchase price limits, and eligible counties vary by program. A local lender familiar with Ohio programs can help you determine what you may qualify for.

Q.6 Is a fixed-rate or adjustable-rate mortgage better for first-time buyers?

It depends on your timeline and financial goals. Fixed-rate loans offer predictability over the life of the loan. ARMs can offer lower initial payments, which may be attractive if you plan to move or refinance within a set number of years. Both have trade-offs worth discussing with a lender before deciding.